🍞 The Money Games - Part 3

A 5-Part Guide to Earning, Saving, Borrowing, and Investing Money Wisely

Sup Loyal Bread Crumbers 👋🏻,

Remember that annual letter I mentioned a few weeks ago?

What’s that? You’ve been dying to read it?

Well, I’ve heard your prayers and will be releasing it on Sunday, February 11th.

That’s all.

Without further ado…Money Games Part 3!

Introduction

For all the newbies in YM2 town, go back and check out Money Games Part 1 & 2.

That’s required reading material. You’re in Money Games 301 territory. Don’t skip the pre-recs, dummy.

For this essay, I needed help from “The Don” of personal finance, Ramit Sethi. Ramit’s irreverent tone and practical advice make him the GOAT. He’s a no-bullshit Stanford-educated dude who wrote a New York Times Best Seller, and then spent 20 years writing on the internet about personal finance.

His book, I Will Teach You To Be Rich, is my bible. I suggest you buy a copy and make it yours. This essay uses it as source material. If you hate this essay, blame me, not Ramit. With that said, let’s get started.

Money Problems

Why do you suck at money? I don’t mean that pejoratively. I mean it statistically.

77% of Americans report feeling anxious about their financial situation. Are you part of this sad group? You’re not alone. Before reading Ramit’s book, I had 99 problems and money was certainly one.

Ironically, I majored in finance at the University of Illinois, graduated with a 3.8 GPA, worked in investment banking, lent money professionally, and still sucked at personal finance. Why?

Money is an emotional topic. Personal finance is one part math and two parts psychology. We each have a unique set of (largely irrational) beliefs about money. Many of these beliefs were instilled in us as children. With practice, we can overcome them.

The first step is to stop making excuses. Some of you might be reading this and saying “Why didn’t I learn all this personal finance stuff in school? The U.S. education system let me down. Ugh!”

Tough cookies, crybaby. If you wanted to learn about it, you would have. No college professor taught you how to chug a beer in 20 seconds…but you somehow figured that one out??

Some subjects must be learned outside the classroom. Stop complaining and buckle up buttercup. It’s time to talk credit cards.

Credit Cards - Don’t F*ck Around & Find Out

If personal finance is a playground, credit card companies are the school bullies. They’re strong and aggressive. If you piss them off, your ass is grass. If they respect you, you’ve got great protection. Credit card companies make money off ignorant people. Their weapon of choice? Interest.

These companies lend people money. In return, they charge a fee called “interest”. It’s the cost of borrowing money. Interest is like rent but for money. Credit cards happen to be the most hardcore. A mortgage or student loan might charge 5-7% interest. Credit cards charge over 20%.

At first, interest expenses seem manageable. If you spend $100 on your credit card but can’t afford to pay it back, you’ll be charged 1.7% per month (20% / 12) on your unpaid balance. That means you owe the $100 of principal (what you borrowed) and $1.7 of interest. You now owe $101.7 for borrowing $100. You might think, “…well that’s not so bad.”

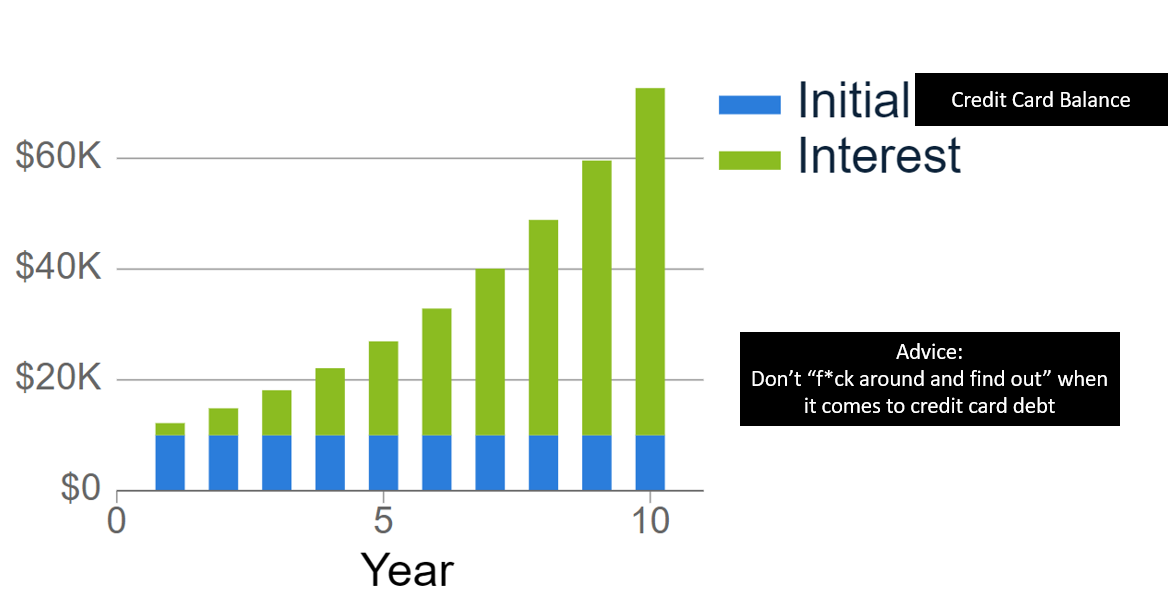

What you fail to see is how quickly that interest can add up. It grows exponentially (that’s very fast). Here’s a simple graph to show how an unpaid balance of $10,000 can add up over time.

In a matter of 10 years, the amount owed goes from $10,000 to $72,000+. Ouch!

First lesson, pay off your credit card balance each month. Just do it. If you are really in the hole and can’t pay it all off, start climbing. Focus on making a recurring payment each month. Eventually, you’ll work your way to paying off the whole balance each month. JUST. GET. STARTED.

Credit cards are a (financial) tool. They should not be avoided. They should be used wisely. It’s like a chainsaw. It’s only dangerous when you don’t know how to handle it. If you learn to use credit cards to your advantage, you can (1) dramatically reduce your borrowing costs (saving you a TON of money) and (2) rack in some sweet cash back and travel rewards.

(1) Reducing Borrowing Costs

By paying down your credit card balance each month, you improve your credit score. A credit score is like a grade for you as a borrower. It tells lenders how likely you are to repay your loan. The higher your credit score, the more likely you are to repay. If the lender believes a borrower is a higher risk, she will charge a higher interest rate. Your credit score takes into account 5 factors. Each factor is weighted differently (see below).

Credit Card Score Factors

Payment History (35%) - Paying (at least) your (minimum) balance each month.

Credit Utilization (30%) - This metric measures what % of your credit card limit is used. The higher your utilization, the worse your credit score. If you can increase your limit, your utilization goes down.

Utilization = [$ credit borrowed] / [$ credit limit]

Length of Credit History (15%) - Self-explanatory. The longer the better.

Credit Mix (10%) - This factor proves you can manage different types of debt like student loans, credit cards, and mortgages effectively.

New Credit Inquiries (10%) - If you apply for tons of new credit cards and the lender does a “hard inquiry” (aka looking at your credit history), your score will see a temporary decline. This is more of a short-term issue. Don’t stress too much about this one.

A good credit score can save you thousands in interest expense. For example, a 2% change in the interest rate on a mortgage could save the borrower $140k.

Crap Credit Chris: $300k mortgage loan, 30-year repayment, 7% interest

→**$420k of interest payments**

Great Credit Gary: $300k mortgage loan, 30-year repayment, 5% interest

→**$280k of interest payments**

In addition to reducing borrowing costs, good credit card usage earns you rewards.

(2) Providing Rewards

The competition among credit card companies is fierce. In an attempt to win new business, they offer users rewards. Savvy users (like you) learn to exploit these rewards.

But (and this is a big but) the benefit you get from the rewards is destroyed if you don’t pay off your credit card balance each month. The 20%+ interest rate credit cards charge on unpaid balances outweighs the cash back or travel rewards. If you’re not accruing interest on your credit card, these rewards are free money. The two most common rewards are cash back and travel points.

Cash Back - It’s a pretty simple reward. For every dollar you spend on your credit card, you get ~2% back in cash. If you spent $10,000, you’d be able to redeem $200 in cash. Cards with this reward are good for everyday purchases.

Travel - If you enjoy traveling (and a little credit card jiu-jitsu) these cards are for you. Travel rewards cards follow the same concept as cashback cards, except users accrue points or miles instead of money. These rewards can be redeemed for flights, hotel rooms, and other travel purchases.

Full disclosure, I do not have a travel card right now but plan to get the Chase Sapphire Reserve. I currently use the Chase Freedom card as my cash-back card. Ramit uses the Fidelity 2% cash back card and the Chase Sapphire Reserve (for travel). One last tip for making the most of credit card exploitation - use the services no one tells you about.

Most credit cards include these benefits (for free) but hide them in the fine print. All it takes is one call to the credit card company and you’ve saved yourself thousands of dollars.

Trip cancellation insurance for flights (usually up to $10,000 per trip)

Rental car insurance (usually up to $50,000)

Extend manufacturer warranties for up to 5 years (replace those broken Bose headphones)

Taking advantage of your credit cards (as opposed to them taking advantage of you) is a huge W. Cast off the ridiculous notion that you are a victim at the whim of these companies. You’re better than that! With the credit card monster handled, we can move to bank accounts.

Checking Accounts

Most people only need two types of bank accounts, checking and savings. A checking account makes your money easily accessible. You can swipe a debit card, transfer funds, write a check, or visit an ATM.

For the athletically inclined, a checking account is like a point guard. It’s in charge of handling the basketball, setting up the offense, and dishing out assists. The first stop for your paycheck is your checking account. From there, that money will be dished out for rent, student loans, credit card payments, other expenses, and investing/savings goals.

Ramit recommends automating these checking account activities. By doing so, you free up brain power for more interesting stuff. Even a finance nerd like me hates constantly thinking about moving my money around. You might be hesitant to do this because you fear you’ll end up with a negative balance.

I had this fear as well but if you spend just a few hours writing down the numbers and the timing of the cash flows, you’ll prevent it from happening. And even if it does happen, it’s not the end of the world (I’ve been there and survived). If you still don’t feel comfortable, keep a few hundred bucks in the account as a margin of safety.

Here’s how my checking account system is set up.

Paul’s Checking Account System

31st of the Month N:

Contribute 5% of gross pay (my employer matches up to 5%) to employer 401k (we’ll talk more about 401ks in Money Games Pt. 4)

My paycheck is direct deposited into my Chase checking account

1st of Month N+1:

Rent payment is automatically sent from my Chase checking account

Utility payment is automatically sent from my Chase checking account

15th of Month N+1:

Contribute 5% of gross pay to employer 401k

My paycheck is direct deposited into my Chase checking account

17th of Month N+1:

Automatic transfer of $[A] to Capital One high-yield savings account (more about this in a sec)

Automatic transfer of $[B] to pay off Chase credit card balances (avoid the interest monster 🙂)

Automatic transfer of $[C] to my Vanguard Roth IRA (more about this in Pt. 4)

If you still have money left over after hitting your savings goals (more about this below), paying off credit cards, and maxing out your Roth IRA, go back and max out your 401k. If you still have money after that (congrats on being rich), look into maxing out your Health Savings Account. If you still have money left over after maxing out your HSA (maybe give me some?) you can open a non-retirement investment account. I’d avoid becoming a day trader but I mean do what you want.

Enough about investment accounts, we are getting ahead of ourselves. We’ll dive into those in Part 4. We need to get back on track. We need to talk about your savings account.

Savings Accounts

Unlike checking accounts, savings accounts aren’t set up for lots of activity. Think of your savings account like those big vaults at Gringott’s Bank from Harry Potter. What goes in, is not supposed to come out for a while.

Ramit recommends setting up your checking and savings accounts at different banks. Why? If your checking account is at Chase but your savings account is at Capital One, it will take 2-3 business days to transfer funds from your savings account to your checking account. That little bit of friction creates better decision-making. You are less likely to spend money you can’t access immediately.

The quicker the cash leaves your checking account (for your savings account), the less likely you’ll spend it impulsively. It’s simple psychology. Temptation reduction. It’s why people trying to get healthier avoid buying junk food. It’s easier to avoid binging on junk food when you don’t have any.

There are two reasons for putting cash into a savings account. First, the account is a good tool when saving for short-term financial goals. Maybe you are setting aside money for a wedding, a vacation, a down payment, or some other large purchase you expect to make in the next 5 years.

Second, it’s a good spot for your Emergency Fund. When some unforeseen event leads to a loss of income (losing a job) or a large expense (medical issue) your Emergency Fund is there to save the day. Many Americans can’t afford an unexpected $1,000 expense.

Ramit suggests having enough cash in your Emergency Fund to pay for 3-6 months of living expenses. Why? It takes people, on average, 3-6 months to find a new job. Personally, my goal is to have 12 months saved. To me, the peace of mind created by 12 months of Emergency Funds is worth the effort and investment.

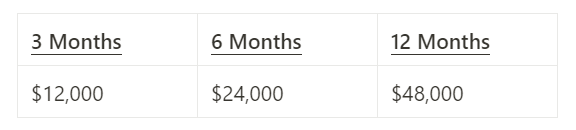

Here’s some quick math to give you a ballpark idea of how much cash you’ll want in your Emergency Fund. I’m assuming if times get tough, you could live on $4,000 per month. That $4,000 would cover rent + utilities + food + transportation + insurance + other mandatory expenses.

It’s okay if you don’t have an Emergency Fund yet! Getting to $24,000 or $48,000 might seem impossible today but just getting started makes you a winner. If you can save an extra $200/month, you’ll be halfway to $24,000 in 5 years. If you can save $400/month you’ll be at $24,000 in 5 years. If you can save $600/month you’ll be there in 3 years.

To get the most out of your short-term savings goals and Emergency Fund, open a “high-yield savings account”. It’s like a regular savings account but, you guessed it, provides higher interest yields. These accounts are typically offered by online banks. I use the Capital One 360 Performance Savings. Today (01/28/24), this account offers you 4.35% yearly interest on your savings (this rate will likely come down). That means if you had $10,000 in the account for a year, the bank would pay you $435 in interest. For context, a regular savings account would have paid you $35.

I’d like to end this essay on an uplifting note. We’ve gotten in the weeds on credit cards, interest rates, checking accounts, savings accounts, and emergency funds. These topics can feel overwhelming (and boring) at times. But getting a handle on them enables you to focus on what will bring you joy, living a rich life. A rich life is a term I’ve stolen from Ramit’s book.

It’s a life where we spend time and money on the things we care about. Creating a rich life starts with getting the boring (but essential) stuff automated. The next step is to determine how much money we can spend “guilt-free” each month. To find that number, Ramit suggests creating a conscious spending plan.

Conscious Spending & Living a Rich Life

Conscious spending is based on a simple principle. Saying “no” to spending money on things you don’t care about and “yes” to things you do. Do you want to get an appetizer at dinner? The conscious spending plan says, “Okaaaayyy! Go ahead, queeeeeeeen!”

The first step in the conscious spending plan is identifying your categories of spending. I like to break them up into 4 major sections.

Fixed Costs (Rent, Utilities, Food, Debt, Health, etc.) - These are the expenses you have to pay to be a productive member of society. Add these costs up for a month (Nerdwallet or Empower can do this for free) and divide them by your monthly paychecks. The expenses should make up 50% - 60% of your monthly paychecks.

Investment Contributions (401k, Roth IRA, etc.) - These are contributions for your future retirement. Typically, you’ll use 5% on your employer 401k match and another 5% on your Roth IRA. So, you’ll probably use about 10% of your monthly income for this category.

Savings Goals (emergency fund, wedding, down payment) - The amount of money you put away for this category will depend on your individual goals. Ramit recommends targeting 10% of your monthly paychecks.

Guilt-Free Spending Money - After using your monthly income for your fixed costs, investment contributions, and savings goals you’ll have about 20% leftover for what I like to call “Fun Money”.

Fun Money is the beautiful outcome of Ramit’s Conscious Spending Plan. The plan prevents your finances from devolving into a flaming pile of trash. Having a plan that prevents you from looking like a clown gives you the confidence to spend that Fun Money like a baller.

Let’s say your monthly take-home pay is $5,000. You’d use $3,000 for fixed costs, $500 for investments, and $500 for savings. That leaves you with $1,000 of Fun Money.

Ramit’s rich life philosophy helps you maximize that Fun Money. Ruthlessly avoid spending your Fun Money on things you don’t care about and splurge on stuff you adore. If you love music, maybe that means paying $400 for a Lollapooloza 4-Day pass. If you love food, maybe it means spending $500 on a 3-Michellin star restaurant. If you love relaxing, maybe that means using $500 for a one-night stay in a beautiful penthouse suite.

The key here is to identify what matters to you. If you love traveling but don’t care about clothes, shop at the Gap and save your Fun Money for an awesome trip to Tokyo. Your rich life might look odd to your friends. That’s fine! They aren’t you!

They might not understand how you can afford a $500 handbag. That’s because they don’t see the tradeoffs you are making. Maybe you bought a $500 handbag but avoid eating out on weekends. That’s living a rich life. The guilt-free spending will empower you not to fear splurging on the things you love. You’ll know that splurging is balanced out by cutting ruthlessly somewhere else AND staying up to date on allocations to your fixed costs, investing contributions, and savings goals.

Closing Remarks

That’s all I’ve got for you today folks. We covered a lot in this essay. Thanks for hanging in there. I’d highly, highly, highly recommend getting Ramit’s book. The book covers all of these topics (and more) in greater detail.

Full disclosure, I’m still trying to figure out what my rich life looks like and how to automate my conscious spending plan. That said, I can tell you firsthand hand it feels soooooo freaking good to just have a plan. The feeling of being financially lost is gone. I hope this essay and Ramit’s book can do that for you. To wrap up, here is a simplified, step-by-step plan for what we covered in this essay.

I’d suggest allocating a few hours over the next few weekends to work through the steps. There isn’t a rush but don’t put it off. It’s well worth the time you have to invest.

Money Games Part 3 Step-by-Step Summary

Set up a checking account (Ramit recommends Charles Schwab or Chime)

Set up a high-yield savings account (Ramit recommends Capital One 360 Performance Savings)

Set up a credit card with cashback rewards (Ramit recommends the Fidelity 2% cash back card) and one with travel rewards (Ramit recommends the Chase Sapphire Reserve card)

If you have credit card debt, pay it off or start setting recurring payments to chip away at it

Download Nerdwallet or Empower (I’ve started liking Empower more) to analyze monthly spending and create a Conscious Spending Plan

Establish automatic transfers in your checking account to pay fixed costs, make investment contributions, and transfer money to your high-yield savings account

Identify where you want to splurge with your Fun Money

Buy Ramit’s book and continue to learn how to build a rich life

I’ll see y’all in the next essay where we will make investing less stressful and more fun.

Have a great week!

Cheers,

Paul

P.S. If you are new here, use this button to subscribe…